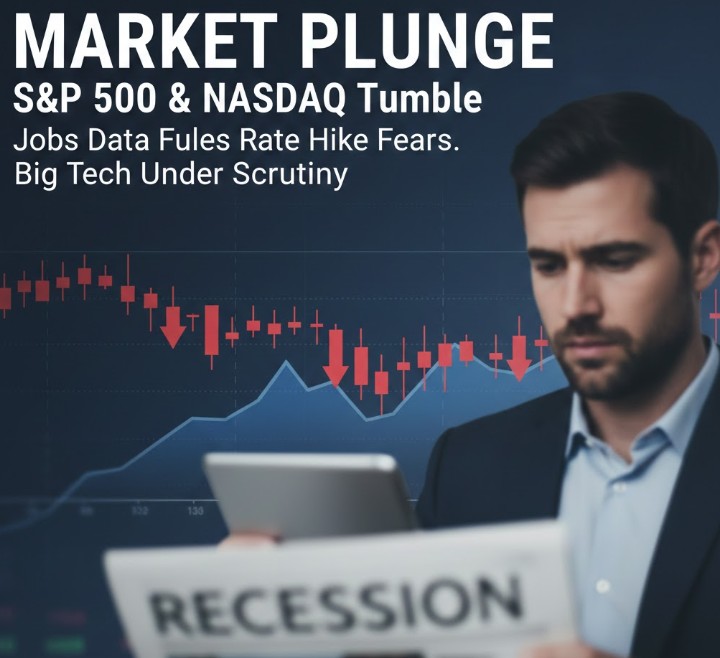

Jobs Data and Big Tech Send S&P 500, Nasdaq Tumbling

The U.S. stock market experienced a

significant downturn, with the S&P 500 and technology-heavy Nasdaq

Composite retreating sharply, including drops of 1.2% and 1.6% respectively on

February 5th. This market decline was primarily catalyzed by stronger-than-expected

jobs data, which fueled concerns about persistent inflation and a more

aggressive Federal Reserve, alongside renewed investor apprehension regarding

the valuation and future growth prospects of "big tech" giants. The

confluence of macroeconomic indicators and sector-specific pressures has

effectively shifted market sentiment, leading investors to re-evaluate risk and

growth trajectories.

Background:

A Market at a Crossroads

Prior to the recent sell-off, the stock market

had been navigating a period of uncertainty, often described as being "at

a crossroads." Investors were grappling with mixed signals: persistent

inflation data on one hand, and resilient corporate earnings and economic

growth on the other.

The S&P 500 had been attempting to sustain

upward momentum, with the Nasdaq benefiting from the perceived stability and

innovation of large technology companies. However, this delicate balance was

predicated on a benign outlook for inflation and interest rates, which now

appears to be under threat.

The technology sector, in particular, had

enjoyed a robust period of growth, often leading broader market rallies, making

it especially sensitive to shifts in the economic narrative.

Detailed

Analysis: The Dual Catalysts for Decline

The primary drivers behind the market's recent

retreat stem from two interconnected forces: robust jobs data and a

re-evaluation of the "big tech" sector.

Firstly, recent employment figures have

indicated a surprisingly resilient labor market, far exceeding economists'

expectations. While strong employment numbers typically signal a healthy

economy, in the current inflationary environment, they paradoxically become a

source of concern for investors.

A tight labor market often translates to

higher wage growth, which can, in turn, contribute to persistent inflation.

This strengthens the case for the Federal Reserve to maintain or even

accelerate its hawkish monetary policy stance, potentially leading to further

interest rate hikes.

Higher interest rates increase the cost of

borrowing for companies and consumers, cool economic activity, and reduce the

present value of future earnings, hitting growth-oriented sectors like

technology particularly hard. The market's fear is that the Fed might be

compelled to engineer a "hard landing" to curb inflation, a scenario

that significantly increases the risk of a recession.

Secondly, the "big tech" sector,

which comprises the largest and most influential technology companies, played a

crucial role in the market's decline. These companies, often characterized by

high growth potential and significant market capitalization, are particularly

sensitive to interest rate fluctuations due to their valuation models heavily

relying on future earnings projections.

As interest rates rise, the discount rate

applied to these future earnings increases, diminishing their present value and

making their current stock prices appear less attractive. Furthermore, concerns

about regulatory scrutiny, slowing growth in certain segments post-pandemic

surge, and intensified competition are all contributing factors.

While specific company news was not cited, the

general apprehension around the sustainability of "big tech"

valuations in a rising rate environment spurred widespread selling pressure

across the sector, given its substantial weighting in indices like the Nasdaq

Composite and, increasingly, the S&P 500. The market's dependency on these

giants means that any weakness in their performance or investor sentiment

towards them can have an outsized impact on the broader market.

Market

Reaction and Expert Commentary

The immediate market reaction to these

catalysts was swift and decisive. The S&P 500's 1.2% drop and the Nasdaq's

1.6% decline on February 5th underscore the sensitivity of investor sentiment

to both macroeconomic data and sector-specific headwinds.

Analysts across Wall Street have begun to

articulate a more cautious outlook, emphasizing the challenges posed by a

hawkish Federal Reserve and potentially stretched valuations in certain growth

sectors. Many strategists now point to the need for investors to recalibrate

their expectations regarding the trajectory of interest rates.

"The robust jobs report has essentially

pushed back the timeline for any potential Fed pivot, suggesting that 'higher

for longer' is still the prevailing mantra," noted one prominent

economist.

Furthermore, investment banks are issuing

revised price targets for technology stocks, with some analysts highlighting

that even fundamentally strong companies may face headwinds purely from a

valuation perspective in a rising rate environment. The consensus appears to be

shifting towards a recognition that the market may experience increased

volatility as it digests the implications of sustained inflation and a

determined central bank.

What This

Means for Investors: Actionable Insights

- Re-evaluate

Growth Stock Exposure: Investors with significant exposure to

high-growth technology stocks should assess their risk tolerance and

potentially consider rebalancing portfolios. While long-term growth

stories remain compelling, near-term volatility driven by interest rate

sensitivity could persist.

- Focus

on Fundamentals and Value: In a rising rate environment, companies

with strong balance sheets, consistent free cash flow, and more reasonable

valuations may offer greater resilience. A shift towards value-oriented

stocks or dividend-payers could provide a defensive posture.

- Monitor

Economic Data Closely: Employment reports, inflation figures

(CPI, PPI), and Fed commentary will continue to be paramount. These data

points will directly influence monetary policy and, consequently, market

direction.

- Consider

Diversification Beyond Equities: Investors might explore diversifying

into assets that traditionally perform well during periods of inflation or

rising rates, such as commodities or certain real estate sectors, although

careful due diligence is essential.

- Embrace

Long-Term Perspective: While short-term volatility can be

unnerving, maintaining a long-term investment horizon and sticking to a

well-defined financial plan is crucial. Panic selling during downturns

often leads to missed opportunities during subsequent recoveries.

Conclusion:

Navigating a Volatile Landscape

The recent market sell-off, driven by

unexpected strength in the labor market and renewed anxieties surrounding

"big tech" valuations, serves as a potent reminder of the complex

interplay between macroeconomic forces and market performance.

As the Federal Reserve continues its battle

against inflation, the path forward for equity markets is likely to remain

volatile, characterized by periods of uncertainty and sharp corrections.

Investors must remain vigilant, adapting their strategies to an environment

where interest rates are likely to stay elevated for longer than previously

anticipated, and where sector leadership may evolve.

A disciplined approach, grounded in

fundamental analysis and prudent risk management, will be paramount for

navigating these evolving market dynamics and securing long-term financial

success. The ability to identify resilient companies and diversify effectively

will be key to weathering the ongoing macroeconomic headwinds.

The U.S. stock market declined due to strong

jobs data fueling fears of persistent inflation and aggressive Federal Reserve

rate hikes, alongside renewed concerns over big tech valuations.