JPMorgan Earnings Kickoff: Trading Strength Offsets Consumer Pain

JPMorgan Chase kicks off the U.S. bank

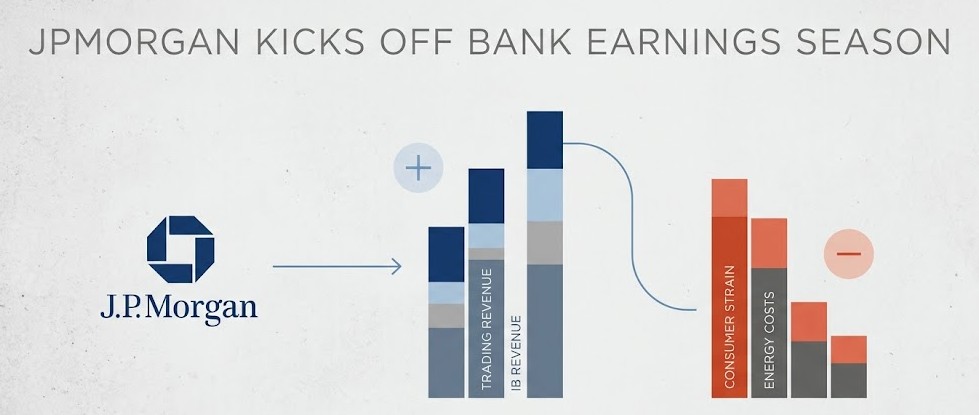

earnings season with first-quarter results expected to show resilient

investment banking and trading revenue, even as higher energy costs weigh on

consumers. The report will be closely read as a gauge of whether banks can

deliver fee-driven growth to offset pressure on consumer spending and loan

performance.

Company

Background and Recent Performance

JPMorgan Chase & Co., the largest U.S.

bank by assets, operates a diversified franchise spanning consumer banking,

corporate and investment banking, asset and wealth management, and treasury

services.

Over the past year, the firm has benefited

from wider net interest margins as the Federal Reserve raised interest rates.

At the same time, its corporate advisory and markets businesses have fluctuated

in line with deal activity and market volatility. Investors will be watching

whether this mix continues to support solid revenue growth and whether

management updates guidance on credit trends and expense control.

Key Drivers

Heading Into Earnings

The primary catalyst for investor attention is

the bank’s investment banking and trading performance. Strong equity and debt

underwriting, merger advisory fees, and activity in fixed income and equities

trading can significantly boost quarterly revenue, particularly during periods

of heightened market activity.

However, rising energy prices and increased

consumer costs present a counterbalancing risk. These factors can reduce

discretionary spending and increase delinquencies on consumer loans and credit

cards, creating headwinds for retail banking operations.

Analyst

Expectations and Market Positioning

Analysts approach the earnings season with

cautious optimism. Many expect strength in trading and underwriting fees to

offset softness in consumer card spending, resulting in a net positive impact

on revenue.

That said, estimates remain sensitive to

management guidance on net interest income, loan growth, and provisions for

potential credit losses. Commentary on corporate deal pipelines, treasury

flows, and consumer credit trends will likely influence stock performance in

the days following the release.

Market behavior so far reflects a balance

between optimism in wholesale banking and concern over consumer health. Bank

stocks have rallied when strong trading results were anticipated but have also

pulled back when lenders flagged weakening retail trends or increased credit

provisions.

Key Metrics

to Watch

Beyond headline figures, several critical

metrics will shape investor interpretation of the results.

Net interest income remains a central driver,

with its trajectory dependent on loan growth and deposit pricing dynamics.

Trading revenue, while potentially strong, tends to be volatile, making

year-over-year comparisons more meaningful than sequential changes.

Credit quality indicators, including

charge-off rates, delinquency levels, and loan loss reserves, will provide

insight into whether rising costs are translating into financial stress for

consumers.

Expense management is another focal point.

JPMorgan has invested heavily in technology and compliance, and while these

investments support long-term growth, sustained profitability requires

disciplined cost control. Any indication of rising expenses could weigh on

sentiment, while signals of margin stability would be viewed positively.

Capital

Allocation and Strategic Focus

Investors will also look for clarity on

capital management, including share buybacks and dividend policy. JPMorgan’s

strong capital position, reflected in its CET1 ratio and liquidity levels, has

historically supported shareholder returns. Any changes in capital allocation

strategy will be closely scrutinized.

Additionally, fee-based and digital businesses

such as asset management and card processing provide recurring revenue streams

that help offset cyclicality in trading and lending operations.

Investor

Considerations

Investors approaching the earnings release

have several strategic options. Conservative investors may choose to wait for

full results and management commentary before adjusting positions, reducing

exposure to short-term volatility.

More active investors anticipating strong

trading performance may consider modest position sizing or hedging strategies

to manage downside risk while retaining upside potential.

Long-term investors focused on income and

capital returns should evaluate the sustainability of dividends and buybacks as

indicators of financial strength and management confidence.

Risks and

Outlook

Key risks include elevated energy prices and

persistent inflation, which could weaken consumer credit performance and lead

to higher loan loss provisions. Broader macroeconomic uncertainty, including

slowing growth or market disruptions, may also impact the bank’s performance.

On the upside, continued strength in corporate

deal activity or increased market volatility could drive stronger-than-expected

trading revenue.

Conclusion

and Forward Looking Perspective

JPMorgan’s first-quarter results will serve as

an early indicator of how the banking sector is navigating a complex economic

environment. The balance between trading and investment banking strength, net

interest income trends, and consumer credit conditions will be central to the

outlook.

While fee-based and trading revenue can offset

consumer-related pressures in the near term, the sustainability of this balance

will determine whether JPMorgan can maintain steady earnings growth in the

quarters ahead.

Market focus remains on whether strong trading and investment banking performance can counter consumer pressure from rising energy costs and shape first-quarter revenue and forward guidance.