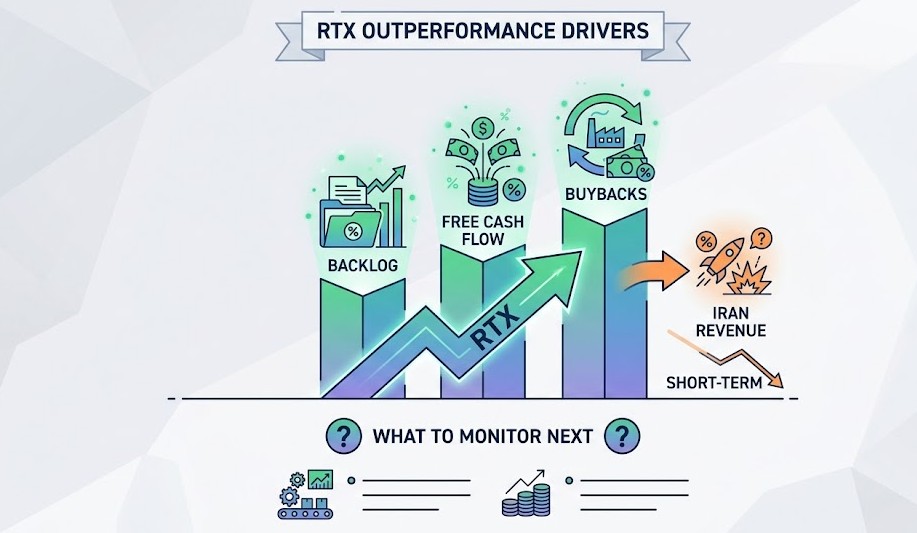

RTX Outpaces Market After Iran Shock: Why Investors Are Taking Notice

RTX Corp. shares have outperformed the broader

market in recent sessions, even as the conflict in Iran has not translated into

immediate revenue gains for large-cap defense contractors. Investors appear to

be pricing in the company’s durable backlog, improving free cash flow, and

shareholder-friendly capital deployment rather than near-term boosts from

geopolitical tensions.

Background

and Recent Performance

RTX (ticker: RTX) is a diversified aerospace

and defense conglomerate formed from the merger of Raytheon and United

Technologies. Its principal businesses include Pratt & Whitney jet engines,

Collins Aerospace systems, and Raytheon Missiles & Defense, generating

revenue from commercial aviation, military platforms, and long-term service

contracts.

Over the past several quarters, the company

has focused on margin improvement, cost reduction programs, and steady cash

returns to shareholders through dividends and buybacks. Its large government

backlog and multiyear contracts provide revenue visibility that appeals to

investors during periods of uncertainty.

At the same time, RTX’s exposure to commercial

aviation ties its performance to airline demand and aircraft production rates,

which can dampen the impact of short-term geopolitical demand for weapons. This

dynamic helps explain why a sudden escalation abroad may not produce a rapid

revenue windfall for an integrated supplier like RTX.

Analysis of

the Recent News Event

Recent coverage highlighted that the Iran

conflict has not directly improved RTX’s near-term order flow, underscoring

that defense procurement typically moves on budgetary and programmatic

timelines rather than immediate crisis response.

New foreign military sales, congressional

appropriations, and multi-year procurement agreements generally unfold over

months to years, with many major programs already committed under existing

contract schedules.

Instead, the current situation appears to have

accelerated a sector re-rating. Investors have rotated into large,

cash-generative defense names as a hedge against market volatility, favoring

companies with stable cash flows, robust backlogs, and visible capital return

policies.

For RTX, this has meant multiple valuation

drivers beyond immediate contract wins, including a large installed base

supporting high-margin services, disciplined cost control, and a capital

allocation strategy that has returned significant value to shareholders through

dividends and buybacks. Investors should review the latest company filings for

precise figures.

Beyond headline developments, key operational

indicators to monitor include quarterly margin expansion, free cash flow

conversion, procurement wins in missile systems and avionics, and commercial

engine order trends. Supply chain pressures and labor constraints remain risks

that could delay revenue recognition and compress margins, making progress on

manufacturing throughput and cost control critical.

Market

Reaction and Analyst Commentary

The market has rewarded companies perceived as

reliable cash generators and providers of essential products. Analysts have

increasingly emphasized fundamentals such as free cash flow conversion, backlog

growth, and margin trajectory when revisiting ratings for the aerospace and

defense sector.

Several brokerage notes since the escalation

indicate that while top-line sensitivity to short-term conflicts is limited,

earnings per share upside can still emerge from improved margins, higher

service revenues, and steady defense spending allocations.

Institutional flows into defense-focused ETFs

and large-cap value funds have also supported share prices, tightening

liquidity and compressing spreads. However, some strategists caution that

valuation re-ratings may reverse if macroeconomic conditions shift or if

defense budgets fail to increase as expected.

Investors should monitor updates to

congressional defense budgets, Department of Defense procurement schedules, and

major contract announcements that could materially alter forward revenue

expectations.

What This

Means for Investors

For long-term investors seeking exposure to

aerospace and defense, RTX offers a blend of cyclical and defensive

characteristics. Its sizable backlog and service revenue provide resilience

during commercial aviation slowdowns, while its defense operations benefit from

structural demand linked to national security priorities.

Key considerations for investors include

monitoring free cash flow and margin progress, tracking backlog and

book-to-bill ratios, evaluating capital allocation through dividends and

buybacks, and comparing valuation against peers and historical averages.

Short-term traders should recognize that

geopolitical headlines can drive volatility without materially changing

fundamentals. A staggered approach to building positions, combined with

disciplined entry points based on normalized earnings multiples, may help

manage risk.

Conclusion

and Forward Looking Perspective

RTX’s recent outperformance appears driven

less by immediate revenue gains from the Iran conflict and more by a broader

market rotation into cash-generative, defensible businesses with visible

capital returns.

Looking ahead, the primary drivers of upside

are likely to be continued margin expansion, efficient backlog conversion,

accretive contract awards, and disciplined capital deployment. Over the next 12

to 24 months, these factors are expected to play a more significant role in

shaping performance than short-term geopolitical developments.

RTX shares rose as investors rotated into

defensive aerospace and defense names, prioritizing backlog stability and

capital returns over immediate war-driven revenue impacts.