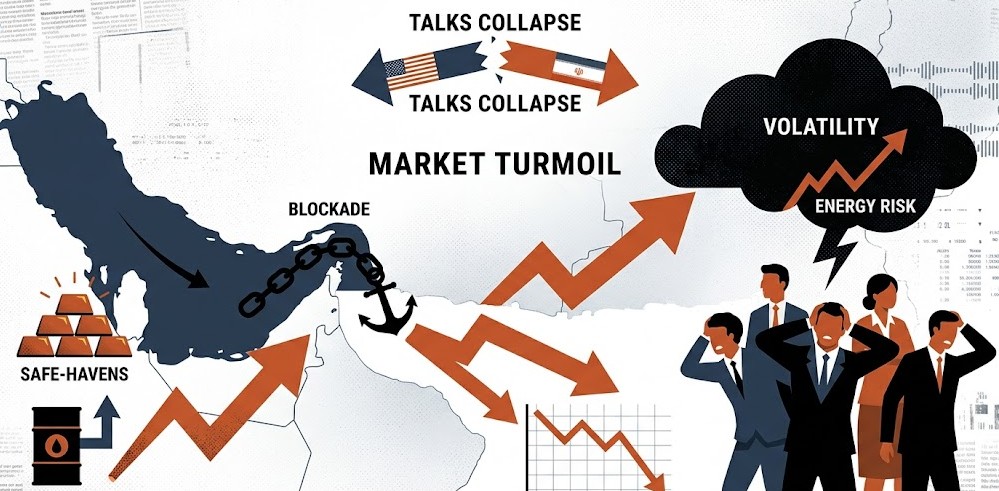

US-Iran Breakdown Sends Futures Lower; Oil, Risk Assets Drop

U.S. equity futures slid Monday after negotiations between the United States

and Iran failed to produce a peace accord and U.S. forces instituted a blockade

near the Strait of Hormuz. The collapse of talks and heightened geopolitical

risk prompted a classic risk-off response, pressuring futures on the Dow,

S&P 500, and Nasdaq ahead of the trading week.

The most direct market proxy for the move is the

SPDR S&P 500 ETF Trust (SPY), which tracks the S&P 500 index and serves

as a flagship barometer for U.S. equity performance. After a year that saw the

broad market recover from last year’s lows, investors had been balancing

resilient corporate earnings against persistent inflation and tighter Federal

Reserve policy expectations.

Geopolitical shocks historically compress risk

appetite, and supply route disruptions in the Middle East carry outsized

implications for energy-sensitive sectors and cyclical names. Monday’s move

reflects two linked transmission channels. First, an abrupt deterioration in

diplomatic prospects raises the likelihood of sustained or escalatory military

activity, increasing the chance of disruption to oil flows through the Strait

of Hormuz, a conduit for roughly one-fifth of seaborne oil trade. Second, the shift

to a risk-off posture pushes investors toward safe-haven assets such as U.S.

Treasuries, the dollar, and gold, while selling growth and cyclically exposed

equities.

For companies with high energy intensity or

profit margins vulnerable to input cost spikes, pressure could intensify if

higher crude prices persist. Commodity markets act as a direct barometer. Even

absent firm intraday data in this bulletin, market practice typically sees a

near-term bid to oil and petroleum products on credible threats to supply

routes. A renewed premium in oil could widen spreads for integrated energy

producers and refineries, while weighing on discretionary spending if fuel

prices rise.

Equity sectors most sensitive to energy and

transport costs, including industrials, airlines, and auto suppliers, warrant

close monitoring. On the trading desk, the decline in equity futures translated

into wider gap-down openings for many names at the cash open, depending on the

magnitude of the premarket move. Market strategists identified geopolitical

risk as the primary driver, compounding concerns about rising energy costs and

potential second-order effects on economic growth.

Several sell-side strategists advised clients

to review exposure to high-beta stocks and consider short-term hedges. Others

emphasized the importance of quality earnings and strong balance sheets in this

environment. Fixed-income markets typically receive inflows during risk-off

episodes, pushing Treasury yields lower and flattening parts of the curve as

investors seek duration. The dollar often strengthens on safe-haven demand,

which can further pressure multinational earnings denominated in foreign currencies.

For portfolio managers, these cross-asset

movements influence hedging costs and the relative attractiveness of U.S.

equities versus international markets in the near term.

Investors may consider reassessing exposure to

energy-intensive sectors and high-beta growth names that could see outsized

downside in a sustained risk-off period. Trimming cyclical positions and

reallocating toward defensive sectors such as utilities, healthcare, and

consumer staples has historically proven effective during heightened

geopolitical risk. Revisiting stop-loss levels and option hedges for

concentrated positions, as well as evaluating fixed-income duration as a

portfolio stabilizer, can also be prudent.

Tax-aware investors may look to rebalance

within taxable accounts to lock in gains where appropriate. Short-term traders

may encounter increased volatility, presenting both risks and opportunities,

making disciplined position sizing and clearly defined exit strategies

essential. Institutional investors should test portfolio stress scenarios under

more adverse oil price and growth assumptions and review liquidity management

plans in light of potential rapid repricing.

It remains important to distinguish between

temporary headline-driven movements and durable shifts in macroeconomic

fundamentals when making allocation decisions. The breakdown in U.S.-Iran talks

and the reported U.S. blockade of the Strait of Hormuz introduce a new layer of

uncertainty that could sustain market volatility. Investors should prepare for

elevated risk premiums, closely monitor oil market signals, and prioritize

liquidity and balance sheet strength in portfolio construction.

Historically, geopolitical flare-ups in the

Persian Gulf have produced short-lived equity selloffs accompanied by spikes in

oil and safe-haven assets, followed by partial recoveries as diplomatic

channels reopen and markets look past temporary supply disruptions. Episodes

such as the 2019 tanker attacks and the 2011 Arab Spring triggered volatility

spikes but caused limited long-term damage to diversified equity portfolios

once shipping insurance and alternative supply lines stabilized.

However, sustained disruptions or escalation

affecting physical flows over an extended period would represent a materially

different scenario, requiring a reassessment of growth and inflation

expectations and likely leading to more persistent sectoral divergence.

Tactically, short-term investors may consider

using options to hedge downside exposure, such as buying protective puts or

establishing put spreads on major indices or concentrated holdings. Longer-term

investors might view market weakness as an opportunity to add high-quality

cyclicals at more attractive valuations if disruptions prove temporary, or to

incrementally increase exposure to energy producers with strong balance sheets

if oil prices stabilize at higher levels.

Maintaining cash buffers and laddered

fixed-income exposure can provide both liquidity and return potential as

volatility stabilizes. Rebalancing strategies should be executed with attention

to tax efficiency and transaction costs.

Stocks and futures fell as U.S.-Iran negotiations collapsed and a U.S. blockade near the Strait of Hormuz heightened geopolitical and oil supply risks, triggering a broad risk-off shift in global markets.