Why Intuit’s Shares Slid Despite AI Leadership — What Investors Should Know

Intuit Inc. (INTU), the software company

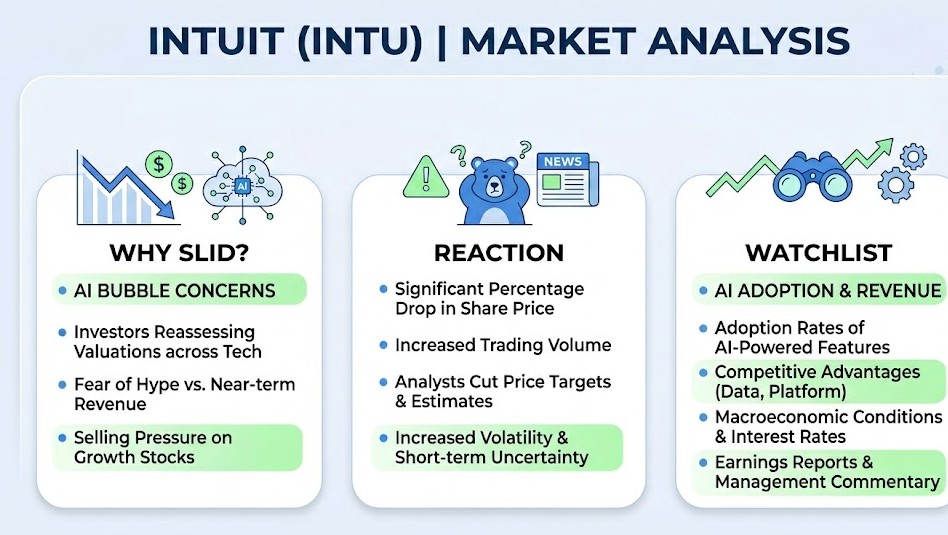

behind TurboTax, QuickBooks, and Credit Karma, saw its shares decline sharply

in a broad selloff targeting high-valuation software names, even as the company

positions itself as an early adopter of artificial intelligence across its

products. Investors reacted to heightened sensitivity around growth and margins

in the software sector, turning a narrative of AI leadership into a near-term

pressure point for a richly valued SaaS company.

Company

Background and Strategic Positioning

Intuit has spent several years embedding

machine learning and AI capabilities into its core offerings. The company

introduced AI-driven tax guidance within TurboTax, conversational assistance

and automation features in QuickBooks, and expanded its consumer finance

presence through the 2020 acquisition of Credit Karma for approximately $7.1

billion.

In 2021, Intuit also acquired Mailchimp for

around $12 billion to strengthen its small-business ecosystem. These

initiatives support its positioning as an AI-enabled platform, combining data,

workflows, and machine learning models to automate processes and personalize

financial outcomes.

Market

Reaction and Recent Selloff

Despite these strategic investments, the

recent stock decline highlights investor concern over near-term execution and

valuation. Intuit trades at a premium compared to many software peers due to

its recurring revenue model and historically strong operating margins. However,

that premium makes it vulnerable to any signals of slowing revenue growth,

rising AI-related investment costs, or weakening demand from small businesses.

The selloff was driven in part by a broader

market rotation favoring a narrower group of perceived pure-play AI companies.

This shift has led investors to reassess established SaaS firms, particularly

those requiring continued investment to maintain competitive positioning.

AI

Narrative and Competitive Debate

The core debate centers on whether Intuit’s AI

capabilities represent a durable competitive advantage or incremental

enhancements requiring ongoing heavy investment. Some market participants argue

that the increasing availability of large language models and commoditized AI

infrastructure could reduce differentiation.

Others highlight Intuit’s strengths, including

its proprietary tax and financial data, integrated product ecosystem, and

advisory network, as defensible advantages that are difficult to replicate.

Analyst

Perspectives and Key Metrics

Analyst sentiment remains mixed. Some have

reduced near-term earnings expectations, citing potential headwinds in

small-business software adoption, payroll services, and customer acquisition

trends.

Conversely, other analysts emphasize Intuit’s

long-term strengths, including high customer retention, cross-selling

opportunities across its platform, and the potential to monetize AI-driven

features to increase customer lifetime value.

Investors are closely monitoring key

performance indicators such as annual recurring revenue growth, gross margin

trends, customer acquisition costs, and AI-related operating expenses to assess

how effectively investments translate into revenue.

Sector

Rotation and Valuation Reset

The market response reflects both

macroeconomic caution and a broader re-rating of software valuations. Investors

have shifted capital toward companies perceived as more directly exposed to

AI-driven growth, funding these moves by reducing exposure to diversified

software names like Intuit.

This has resulted in increased volatility

across the sector, particularly for companies with elevated valuation

multiples. The pullback in Intuit shares should be viewed within this broader

context of changing market preferences and expectations.

Investor

Takeaways

The recent decline offers several

considerations for investors. Distinguishing between short-term market

movements and long-term fundamentals is critical, as Intuit’s recurring revenue

model and diversified product portfolio remain intact.

Monitoring operational performance over the

coming quarters will be key, particularly subscription growth, customer

retention, and the pace at which AI features contribute to revenue and pricing

power. A sustained improvement in these metrics would support the investment

thesis.

Valuation also plays a central role. A

meaningful correction may present a more attractive entry point if the company

continues to demonstrate strong retention and successfully monetizes its AI

initiatives.

Risk

Management and Strategy

Investors with concentrated exposure may

consider managing risk through position adjustments or hedging strategies to

navigate near-term volatility. Those looking to build positions may benefit

from setting clear entry criteria, such as improved guidance, stronger

recurring revenue growth, or tangible evidence of AI-driven monetization.

It is also important to consider capital

allocation priorities, as increased investment in research, development, and

integration efforts could affect shareholder returns in the near term.

Outlook and

Forward Perspective

Intuit’s long-term outlook depends on its

ability to convert AI investments into measurable customer value, sustained

revenue growth, and stable margins. Its proprietary data across tax, financial,

and small-business domains remains a significant strategic advantage.

In the near term, volatility is likely to

persist as the market evaluates which companies can effectively translate AI

capabilities into profitable growth. Investors should monitor upcoming earnings

reports, management commentary on AI strategy, and integration progress across

recent acquisitions for signs of stabilization.

If Intuit demonstrates clear progress in

monetizing AI features while maintaining margin discipline, investor sentiment

could improve. If not, valuation pressure may continue.

Conclusion

Intuit remains strategically well positioned

but faces a near-term execution challenge. The company must demonstrate that

its AI investments can drive predictable revenue growth and margin expansion.

The recent decline reflects a broader rotation away from premium SaaS names, driven by concerns that AI-related spending and slowing growth could compress valuation multiples.